₹100 Daily SIP: How Much Can You Really Earn in 5, 10, 20 & 30 Years?

A deep-dive into the power of compounding — with real numbers, fund recommendations, and a roadmap for every Indian investor.

What if ₹100 a day — less than the price of a chai and a samosa — could make you a crorepati?

Sounds far-fetched, right? But this is exactly what a ₹100 daily SIP (Systematic Investment Plan) can do when paired with the most powerful force in investing: compounding.

Millions of Indians skip investing because they believe they need large sums to start. The truth is, even ₹3,000 a month — that’s ₹100 per day — invested regularly in a good equity mutual fund can build significant, life-changing wealth over time. The key is starting early and staying consistent.

In this guide, we’ll break down exactly how much a ₹100 daily SIP can earn over 5, 10, 20, and 30 years. We’ll also cover the best fund categories, common mistakes, real-life case studies, and actionable steps to start your SIP today.

- What Is a Daily SIP and How Does It Work?

- ₹100 Daily SIP Returns: The Numbers Explained

- The Magic of Compounding: Why Starting Early Matters

- Best Fund Categories for a ₹100 Daily SIP

- How to Start a ₹100 Daily SIP in India (Step-by-Step)

- Expert Tips to Maximise SIP Returns

- Real-Life Case Study: Rahul’s SIP Journey

- Common Mistakes to Avoid

- FAQs

- Conclusion

What Is a Daily SIP and How Does It Work?

A Systematic Investment Plan (SIP) is a method of investing a fixed amount into a mutual fund at regular intervals — monthly, weekly, or daily. Most Indians are familiar with monthly SIPs, but daily SIPs work on the same principle: you invest a small, fixed amount every market day, and your money buys mutual fund units at that day’s NAV (Net Asset Value).

A ₹100 daily SIP means you invest ₹100 each working day. Since there are roughly 21–23 working days in a month, your monthly investment comes to approximately ₹2,100–₹2,300 per month, or about ₹25,200–₹27,600 per year.

Each time you invest ₹100, you buy units of the mutual fund. As markets rise over time, the value of each unit increases. Your returns are then reinvested to buy more units — which in turn earn more returns. This cycle, repeated over years and decades, is what creates exponential wealth growth.

Daily SIP vs Monthly SIP — Which Is Better?

For a ₹3,000/month budget, the difference in final returns between a daily SIP (₹100/day) and a monthly SIP (₹3,000 once a month) is generally marginal in the long run. Both leverage rupee cost averaging. Daily SIPs offer slightly more averaging due to more frequent purchases, but over 20–30 years, the final corpus difference is typically under 1–2%.

The real advantage of a daily SIP is behavioural: it builds the habit of investing every single day, reducing the temptation to spend that money elsewhere.

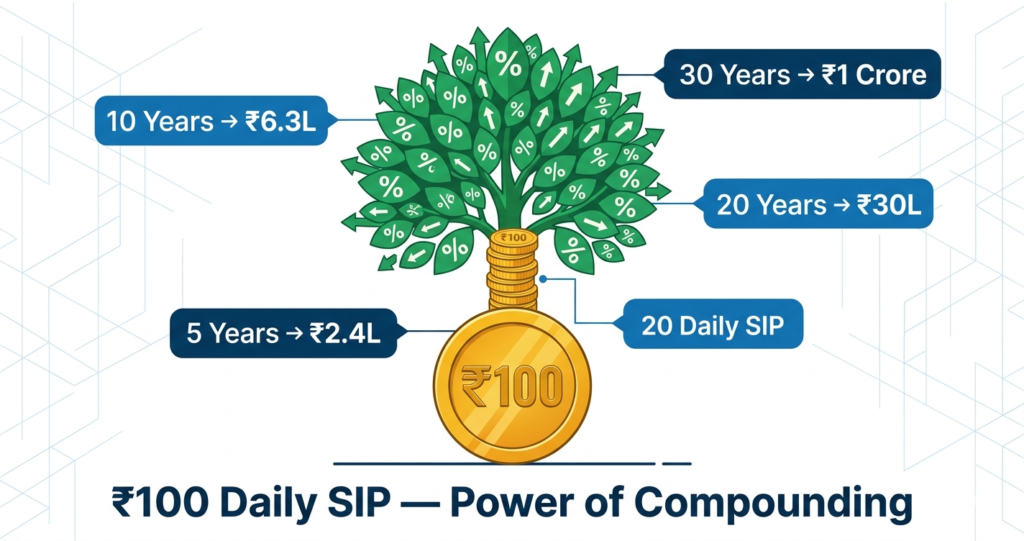

₹100 Daily SIP Returns: The Numbers Explained

Let’s get to the numbers you came for. The table below shows the estimated corpus (wealth) you can build with a ₹100 daily SIP at different return rates — 10%, 12%, and 15% CAGR (Compounded Annual Growth Rate).

Assumption: ₹100 invested per day = ₹3,000 per month (approx). Returns calculated using SIP compounding formula.

| Time Period | Total Invested | At 10% CAGR | At 12% CAGR | At 15% CAGR |

|---|---|---|---|---|

| 5 Years | ₹1.80 Lakh | ₹2.32 Lakh | ₹2.44 Lakh | ₹2.64 Lakh |

| 10 Years | ₹3.60 Lakh | ₹5.73 Lakh | ₹6.29 Lakh | ₹7.44 Lakh |

| 15 Years | ₹5.40 Lakh | ₹12.38 Lakh | ₹15.01 Lakh | ₹20.30 Lakh |

| 20 Years | ₹7.20 Lakh | ₹22.79 Lakh | ₹29.97 Lakh | ₹45.10 Lakh |

| 25 Years | ₹9.00 Lakh | ₹39.78 Lakh | ₹57.10 Lakh | ₹98.60 Lakh |

| 30 Years | ₹10.80 Lakh | ₹67.68 Lakh | ₹1.05 Crore | ₹2.10 Crore |

At 12% CAGR (close to the historical average of top diversified equity funds in India), a ₹100 daily SIP can grow to over ₹1 Crore in 30 years. You invest only ₹10.80 Lakh — but compounding does the rest. At 15% CAGR (achievable with small-cap or flexi-cap funds over long periods), you could accumulate ₹2.10 Crore.

The Magic of Compounding: Why Starting Early Matters

Albert Einstein reportedly called compound interest the “eighth wonder of the world.” Whether or not he actually said it, the math proves the point. In SIP investing, compounding means your returns generate further returns, creating a snowball effect that accelerates over time.

The Cost of Waiting: A 5-Year Delay

Let’s compare two investors — Priya and Rohit — both investing ₹100 per day at 12% CAGR:

| Investor | Start Age | End Age | Years Invested | Total Invested | Final Corpus |

|---|---|---|---|---|---|

| Priya | 25 | 55 | 30 years | ₹10.80 Lakh | ₹1.05 Crore |

| Rohit | 30 | 55 | 25 years | ₹9.00 Lakh | ₹57.10 Lakh |

Priya invested just ₹1.80 Lakh more than Rohit — but ended up with ₹47.9 Lakh more. That’s the price of starting 5 years late. Time, not the amount, is your biggest asset in SIP investing.

Divide 72 by your expected annual return to find how many years it takes to double your money. At 12% CAGR: 72 ÷ 12 = 6 years to double. At 15% CAGR: 72 ÷ 15 = 4.8 years to double. Start early, and your money doubles multiple times over your investing journey.

Best Fund Categories for a ₹100 Daily SIP

Choosing the right fund category is crucial for achieving those 12–15% CAGR returns. Here’s a breakdown of fund categories suited for a ₹100 daily SIP based on risk profile and investment horizon:

1. Large Cap Mutual Funds (Low–Medium Risk)

Large cap funds invest in the top 100 companies by market capitalisation — think Reliance, TCS, HDFC Bank. These are relatively stable and typically deliver 10–12% CAGR over the long term. Suitable for conservative investors or short-to-medium horizons (5–10 years).

2. Flexi Cap / Multi Cap Funds (Medium Risk)

These funds invest across large, mid, and small cap stocks, giving fund managers flexibility to shift based on market conditions. Historical CAGR has been 12–15% over 10+ year periods. Ideal for most SIP investors.

3. Mid Cap & Small Cap Funds (Higher Risk, Higher Reward)

Mid and small cap funds can deliver 15–18%+ CAGR over very long periods (15–20 years), but come with higher short-term volatility. Not recommended for horizons under 7 years. Perfect for young investors in their 20s starting a ₹100 daily SIP.

4. Index Funds (Nifty 50 / Nifty Next 50)

Index funds passively track the Nifty 50 or Sensex. With the lowest expense ratios (0.1–0.2%) and consistent 10–12% historical returns, they are an excellent low-cost option. Warren Buffett recommends index funds for most retail investors globally.

- Age 20–30: 50% Flexi Cap + 30% Mid Cap + 20% Index Fund

- Age 30–40: 40% Large Cap + 40% Flexi Cap + 20% Mid Cap

- Age 40–50: 50% Large Cap + 30% Index Fund + 20% Balanced Advantage

- Age 50+: Reduce equity exposure gradually; shift towards hybrid or debt funds

How to Start a ₹100 Daily SIP in India (Step-by-Step)

Starting a SIP has never been easier in India, thanks to SEBI-regulated platforms and UPI-enabled payments. Here’s how to get started in under 20 minutes:

-

1Complete Your KYC — KYC (Know Your Customer) is mandatory for mutual fund investments. If you already have a Demat account or have invested in any mutual fund, your KYC is likely done. First-timers can complete e-KYC via Aadhaar OTP online at any SEBI-registered KYC Registration Agency (KRA).

-

2Choose a Platform — You can invest via direct platforms like Zerodha Coin, Groww, Kuvera, or Paytm Money (for zero commission direct plans), or via an MFD/distributor. Direct plans have lower expense ratios than regular plans, which means higher returns for you.

-

3Select Your Fund — Based on your age, risk appetite, and investment horizon, pick 1–3 funds from the categories listed above. Avoid investing in too many funds — 2 to 3 well-chosen funds are better than 10 overlapping ones.

-

4Set Up Your Daily SIP — Most platforms allow you to set up a daily SIP of ₹100 or more. Link your bank account via UPI or NACH mandate. The SIP amount will be auto-debited every market day.

-

5Set It and Forget It — The best SIP strategy is to automate and ignore short-term market noise. Review your portfolio once every 6–12 months, not every week.

Expert Tips to Maximise Your ₹100 Daily SIP Returns

If you increase your SIP by just 10% annually — called a Step-Up SIP or Top-Up SIP — the impact on your final corpus is dramatic. Starting at ₹100/day and increasing 10% annually could result in a corpus 2–3x larger than a flat ₹100/day SIP over 30 years.

Many investors panic and stop SIPs when markets fall. This is the worst thing you can do. Market downturns are actually when your SIP purchases more units at lower prices — turbocharging your returns when the market recovers. Stay the course.

Use your annual bonus, tax refund, or any windfall to make a lump sum investment in the same SIP fund. This accelerates your wealth creation significantly without changing your daily routine.

If your ₹100 daily SIP goes into an ELSS (Equity Linked Savings Scheme) fund, you can claim a tax deduction of up to ₹1.5 Lakh per year under Section 80C. With a 3-year lock-in period — the shortest among 80C options — ELSS offers both tax savings and equity market returns.

For SIPs, always evaluate performance using XIRR (Extended Internal Rate of Return), not absolute percentage gain. XIRR accounts for the timing of each investment and gives you the true annualised return on your SIP portfolio.

Real-Life Case Study: Rahul’s ₹100 Daily SIP Journey

📖 Case Study: Rahul, 27, Software Engineer from Pune

Rahul started a ₹100 daily SIP in a flexi cap mutual fund at age 27, after reading about SIPs online. He set up an auto-debit through his savings account via UPI mandate. Here’s what his journey looked like:

- Start Age: 27 | Target Age: 57 (30-year horizon)

- Daily SIP: ₹100 (approximately ₹3,000/month)

- Fund: Diversified Flexi Cap Fund (Direct Plan)

- Average CAGR achieved: ~12.5% (based on category historical average)

- Year 5 corpus: ₹2.5 Lakh (invested ₹1.8 Lakh)

- Year 10 corpus: ₹6.7 Lakh (invested ₹3.6 Lakh)

- Year 20 corpus: ₹32 Lakh (invested ₹7.2 Lakh)

- Year 30 corpus: ₹1.12 Crore (invested ₹10.8 Lakh)

At age 57, Rahul had accumulated over ₹1 Crore from just ₹100 per day. He never earned a windfall. He never picked stocks. He just stayed consistent. Rahul also increased his SIP by 10% every year from age 32, which pushed his corpus further to an estimated ₹1.8 Crore.

Key lesson: Consistency and time, not market timing, create wealth.

Common Mistakes to Avoid with Your ₹100 Daily SIP

A market fall is not a reason to stop your SIP — it’s a reason to celebrate, because you’re buying more units cheaply. Investors who stopped SIPs during COVID-19 crash (March 2020) missed some of the most lucrative buying opportunities in a decade.

Owning 10–15 mutual funds doesn’t reduce risk — it creates portfolio overlap and makes tracking impossible. Stick to 2–4 well-chosen funds. More isn’t better.

Regular plans pay a commission to distributors, resulting in expense ratios 0.5–1% higher than direct plans. Over 30 years, this difference can cost you lakhs of rupees. Always invest in Direct Plans if you’re managing your SIP yourself via Gmfcentral or anyother apps

Investing without a goal leads to premature redemption. Link your ₹100 daily SIP to a specific financial goal — retirement corpus, child’s education, home down payment — and assign a timeline. This makes it emotionally harder to withdraw prematurely.

₹1 Crore 30 years from now won’t have the same purchasing power as today. India’s long-term inflation rate is around 5–6%. Always plan your SIP target corpus after adjusting for inflation. A real-terms target of ₹1 Crore in today’s money means you’ll need roughly ₹4–5 Crore after 30 years of inflation.

Frequently Asked Questions (FAQs)

🏁 Conclusion: The ₹100 Daily Habit That Can Change Your Life

A ₹100 daily SIP is not about the amount — it’s about the habit, the discipline, and the time. The numbers are clear: ₹100 a day, invested consistently for 30 years at 12% CAGR, turns into over ₹1 Crore. Not through speculation. Not through stock picks. Simply through the power of compounding working silently over decades.

Start today. Not next month. Not after your next salary hike. Today. Because in wealth creation, every day you delay is a day of compounding lost forever.

Explore More at Investment Sutras →