Mutual Fund Overlap: The Silent Portfolio Killer

How hidden duplication drains your returns, amplifies risk, and costs you crores in lost compounding — and exactly how to fix it.

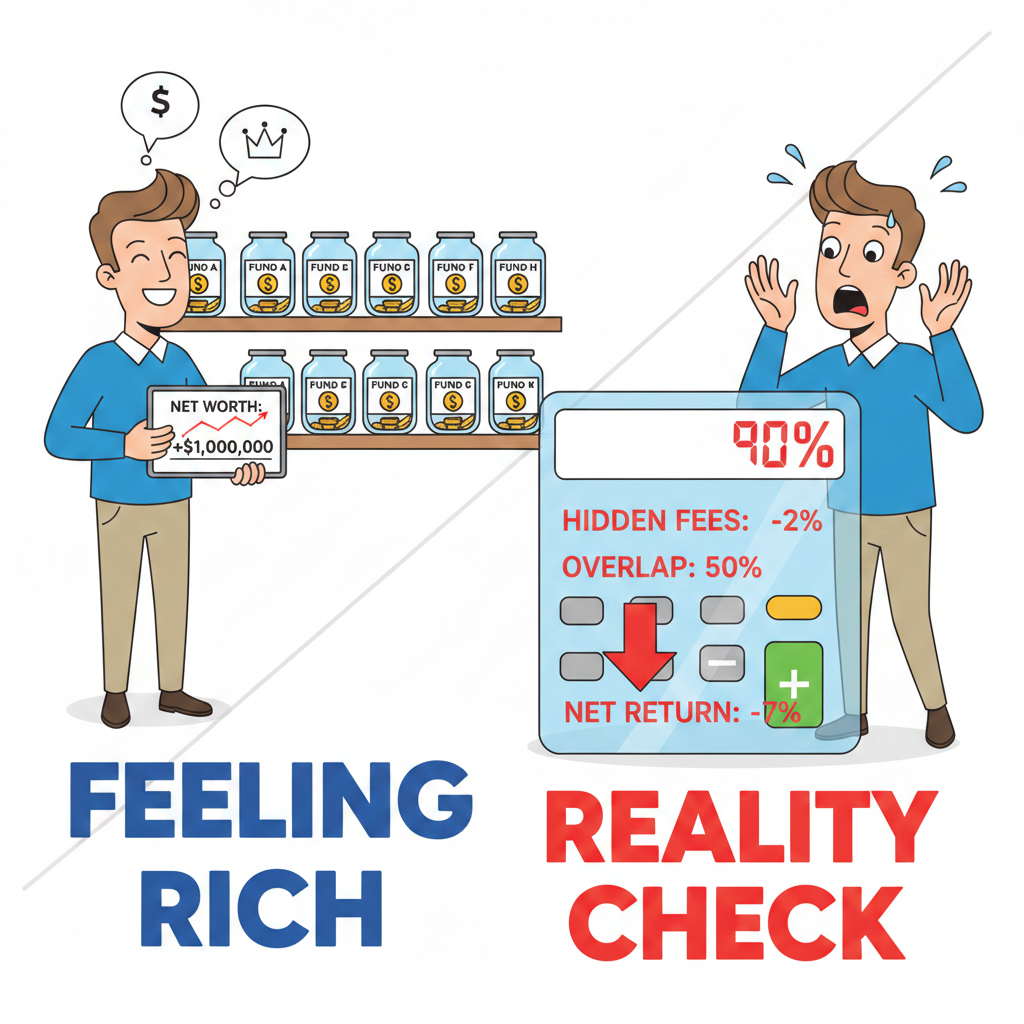

The illusion of diversification is one of the most common—and costly—mistakes in modern investing. You might look at your portfolio and see ten different mutual fund names, congratulating yourself on a job well done. But if you peel back the layers and look under the hood, you might find that those ten funds are really just two or three strategies repeated over and over again. This is the reality of mutual fund overlap, a silent portfolio killer that dilutes your returns, amplifies your risk, and leaves you paying for diversification you never actually get.

In the Indian mutual fund industry, where 428 New Fund Offers (NFOs) were launched in CY2024 alone, the temptation to collect schemes is higher than ever. But as we will explore in this deep dive, a cluttered portfolio is often a weak portfolio.

What is Mutual Fund Overlap?

Mutual fund overlap occurs when two or more schemes in your investment portfolio hold the same underlying stocks or sectors. While the fund names may be different—say, a Large Cap Fund and a Flexi Cap Fund—their portfolios might look strikingly similar. This happens because funds within the same category often chase the same benchmark indices and end up buying the same “blue-chip” darlings like Reliance Industries, HDFC Bank, or Infosys.

The Silent Killers: How Overlap Drains Your Wealth

The damage caused by duplication isn’t always visible on your monthly statement, but it shows up in the long-term trajectory of your wealth. Here is how mutual fund overlap silently erodes your financial future.

1. The Concentration Risk Paradox

You buy five funds to “spread the risk,” but if four of them are heavily invested in the same 10 stocks, you haven’t spread anything. You have simply concentrated your bet across multiple receipts. Consider this example: Imagine you invest ₹2,00,000 split equally between Fund A and Fund B. If both funds carry a 20% allocation in Company X, you effectively have 40% of your total capital riding on that single stock. If Company X falls by 10%, you lose ₹8,000. Had you owned just one fund, the impact would have been half of that. This is the paradox of overlap: you seek safety in numbers, but you actually create a house of cards.

2. The Fee Illusion

Every mutual fund charges an expense ratio. When you hold overlapping funds, you are paying multiple fund management fees for the exact same exposure. As Nikunj Saraf, CEO of Choice Wealth, points out, “Each mutual fund charges its own expense ratio, so when multiple funds hold the same stocks, investors end up paying multiple management fees for similar exposure. This silently eats into returns over long periods.” If you are paying 1% on three funds that are essentially the same, you are paying 3% for a portfolio that could be run for 1%. Over 20 or 30 years, this fee leakage can cost you crores of rupees in lost compounding.

3. False Sense of Security

Perhaps the most dangerous effect of overlap is behavioral. When markets are booming, overlapping funds all go up together, and the investor feels like a genius. But when a downturn hits, the “diversified” portfolio collapses in unison. There is no cushion, no safe harbor, because all the eggs are actually in the same basket.

🔍 Real-world example: In 2023, many mid-cap and small-cap funds held 15–20% of their portfolios in the same top 5 financial stocks. Investors who owned three such funds were effectively betting 50% of their equity on PSU banks. When the banking sector corrected in early 2024, those portfolios bled in unison — true diversification was absent.

Quantifying the Damage: How Much Overlap is Too Much?

Not all overlap is bad. In fact, some level of overlap is unavoidable in a market like India, where the top 20 companies account for a massive portion of the market capitalization. However, there is a threshold where “acceptable” becomes “dangerous.” Financial experts have differing views, but a consensus is emerging around the “Risk Zone” concept:

| Overlap Percentage | Risk Level | Implication for Your Portfolio |

|---|---|---|

| < 20% | Healthy | Funds are genuinely different; true diversification achieved. |

| 20% – 33% | Moderate | Some duplication exists; monitor closely to prevent drift. |

| 33% – 50% | High Risk | Diversification is failing; portfolio behaves like a concentrated bet. |

| > 50% | Critical | Funds are essentially clones; you are paying for redundant exposure. |

* Overlap is usually measured by common stocks or sector weights. Use a portfolio overlap analyzer to get your exact numbers.

How to Detect Overlap in Your Portfolio

If you want to stop the leakage, you need to conduct a portfolio audit. Here is a step-by-step guide to identifying mutual fund overlap.

The Factsheet Method

Download the monthly factsheets for all your mutual funds. Look at the “Top 10 Holdings” or “Top 20 Holdings” section. Create a simple Excel sheet and list the stocks across all your funds. If you see the same names—HDFC Bank, ICICI Bank, Reliance, Infosys—appearing in every single column, you have a red alert.

The Overlap Formula

For a more mathematical approach, use this formula to compare two funds:

Overlap (A,B) = (2 × Number of Common Stocks) ÷ (Total Stocks in A + Total Stocks in B) × 100.

If this percentage is above 20-25%, it’s time to ask some tough questions about why you hold both.

Digital Tools

You don’t have to do all the heavy lifting yourself. Platforms like Morningstar, Value Research, and even brokerage apps like Groww and Zerodha Coin offer portfolio overlap analyzers. You simply upload your holdings or enter your fund names, and the tool will instantly show you the percentage of common stocks and sector-wise concentration.

The Cleanup: How to Prune Your Portfolio Without Losing Money

Identifying the problem is one thing; fixing it is another. You cannot simply panic-sell everything, as you might trigger exit loads and massive tax bills. Here is how to declutter your portfolio intelligently.

1. The “One Champion Per Category” Rule

If you have three large-cap funds, pick the best one. Don’t look just at past returns; look at consistency, fund manager tenure, and expense ratio. Retain the champion and plan an exit from the others.

2. Stopping the Leakage (SIPs First)

Before you sell anything, stop the flow of new money. If you have identified overlapping funds, immediately pause the SIPs in the funds you plan to eliminate. There is no point in buying more of a fund you know you need to sell.

3. Tax-Smart Exits

This is the most critical part. As of FY 2025-26, equity mutual funds held for more than 12 months qualify as Long-Term Capital Gains (LTCG). Gains up to ₹1.25 lakh are tax-free, and anything above that is taxed at 12.5%. Short-term gains (held for less than 12 months) are taxed at 20%. Strategy: If you have a large gain in a fund you want to remove, don’t redeem it all in March. Redeem in tranches. For example, if you have a gain of ₹2.5 lakh, redeem ₹1.25 lakh worth of gains in March 2025 (tax-free) and another ₹1.25 lakh worth of gains in April 2025 (tax-free in the next financial year). This way, you legally avoid tax while cleaning your portfolio.

4. Avoid the Exit Load Trap

Most funds charge an exit load (usually 1%) if you redeem within one year or three months (depending on the fund type). Check the holding period. If you are close to the one-year mark, wait a few months to sell to avoid paying the exit load, unless the fund is fundamentally terrible and you need to exit immediately.

Building a Portfolio with Purpose

The ultimate goal is not to own zero overlapping funds—that’s impossible. The goal is to build a portfolio with intent. Instead of owning 8-10 random funds, aim for 4-6 well-chosen schemes that cover different areas of the market. Consider the Core & Satellite approach:

- The Core (50-70%): Broad market funds like a Nifty 50 Index Fund or a solid Large Cap Fund. This provides stability.

- The Satellites (30-50%): Focused bets like Mid-cap, Small-cap, or Sectoral funds that offer higher growth potential but are inherently riskier.

By ensuring your satellites are truly different from your core, you minimize overlap and maximize the benefit of diversification.

🔑 Key Takeaways

- Mutual fund overlap creates hidden concentration, not diversification.

- You pay multiple expense ratios for the same stocks — a fee drain that compounds against you.

- Overlap above 33% is dangerous; above 50% means your funds are clones.

- Use free online tools to analyze your portfolio today.

- Prune overlapping funds using a tax-efficient, staggered exit plan.

As legendary investor Warren Buffett once said, “Wide diversification is only required when investors do not understand what they are doing.” Take the time this weekend to audit your portfolio. Run the numbers, check the overlap, and cut the dead weight. Your future self—enjoying a streamlined, cost-efficient, and genuinely diversified portfolio—will thank you.