The “Tax Year” vs “Assessment Year” Confusion — Finally Explained for Every Indian Taxpayer

Most Indians file their ITR every year without truly understanding the difference between Financial Year, Previous Year, and Assessment Year. This guide will eliminate that confusion once and for all.

Every year, around July, millions of Indians scramble to file their Income Tax Returns (ITR). The Income Tax portal is buzzing. Chartered accountants’ phones don’t stop ringing. And somewhere in that chaos, someone asks a question that seems embarrassingly simple — but actually trips up even seasoned professionals:

“Wait, is this the Assessment Year 2025–26 or 2026–27? And what exactly is the difference between Financial Year and Assessment Year?”

If you’ve ever filled in the wrong year on your ITR form, received a notice from the Income Tax Department because of a year-related mismatch, or simply felt confused when your CA rattled off terms like “Previous Year,” “Tax Year,” and “AY” interchangeably — this guide is written exclusively for you.

In this comprehensive explainer, you will learn the precise meaning of Tax Year (Financial Year / Previous Year) and Assessment Year, understand the one-year offset between them, see real-life Indian examples, avoid the most common mistakes taxpayers make, and walk away with complete clarity on how these terms affect your ITR filing, advance tax payment, and tax refunds.

📋 Table of Contents

- What is a “Tax Year” (Financial Year / Previous Year)?

- What is an Assessment Year (AY)?

- Key Differences: Tax Year vs Assessment Year

- Why is There a One-Year Gap? The Logic Behind It

- Important Tax Dates: FY 2025–26 and AY 2026–27

- The New “Tax Year” Concept Under the Income Tax Bill 2025

- How FY and AY Apply to Your Investments (SIP, Mutual Funds, LTCG)

- Real-Life Case Study: Riya’s Tax Confusion

- Expert Tips to Never Get Confused Again

- Common Mistakes to Avoid

- FAQs

- Conclusion

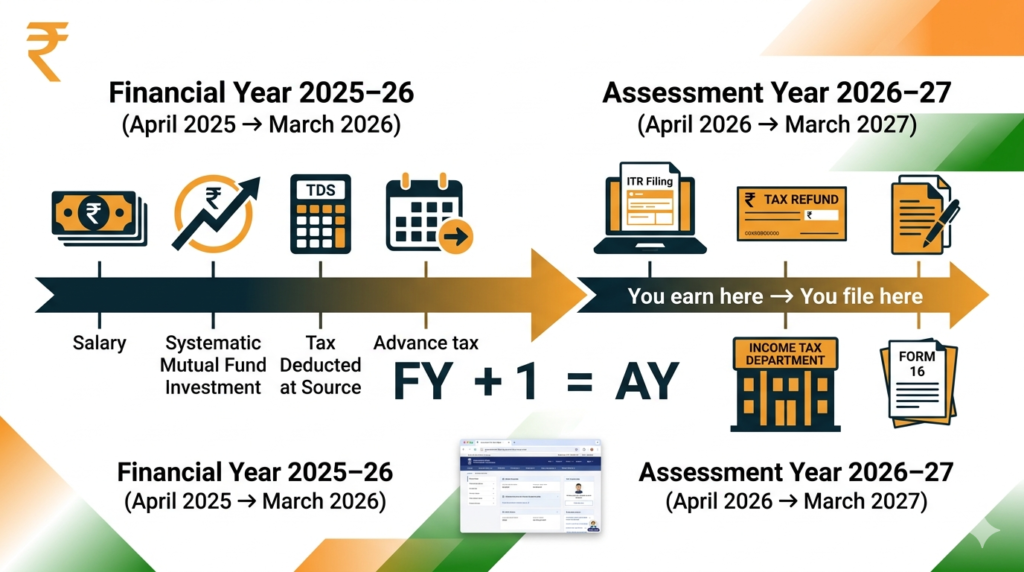

1. What is a “Tax Year” (Financial Year / Previous Year)?

The term “Tax Year” in the Indian context refers to the period during which you actually earn your income. Under India’s Income Tax Act, 1961, this is officially called the Previous Year — the year in which your income is generated. Colloquially and in everyday usage (including government communications), this same period is also called the Financial Year (FY).

In India, the Financial Year runs from April 1st to March 31st of the following calendar year. So:

| Financial Year (FY) | Period | Also Called |

|---|---|---|

| FY 2024–25 | April 1, 2024 – March 31, 2025 | Previous Year 2024–25 |

| FY 2025–26 | April 1, 2025 – March 31, 2026 | Previous Year 2025–26 / Tax Year 2025–26 |

| FY 2026–27 | April 1, 2026 – March 31, 2027 | Previous Year 2026–27 |

The term “Previous Year” was coined by the Income Tax Act to indicate that the year being taxed is the year previous to the year of assessment. It can sound confusing because when you’re filing in 2025, you’re filing for the year that just ended — your income from April 2024 to March 2025.

What Happens During the Tax Year / Financial Year?

- You earn your salary, business income, rental income, interest, capital gains, etc.

- Your employer deducts TDS (Tax Deducted at Source) from your salary monthly.

- You invest in tax-saving instruments like ELSS, PPF, NPS under Section 80C.

- If you’re a freelancer or businessperson, you pay Advance Tax in instalments.

- All these transactions happen during the Financial Year.

2. What is an Assessment Year (AY)?

The Assessment Year (AY) is the year immediately following the Financial Year — the year in which the Income Tax Department assesses and evaluates the income you earned in the previous Financial Year. This is when you file your Income Tax Return, pay any remaining tax dues, and the government processes your tax liability.

Think of it this way: You work and earn income all through FY 2025–26 (April 2025 to March 2026). Once the year ends, you sit down in the next year — AY 2026–27 — to calculate, report, and pay your taxes on that income.

| Assessment Year (AY) | Corresponding Financial Year | ITR Filing Deadline (Typically) |

|---|---|---|

| AY 2024–25 | FY 2023–24 | July 31, 2024 (individuals) |

| AY 2025–26 | FY 2024–25 | July 31, 2025 (individuals) |

| AY 2026–27 | FY 2025–26 | July 31, 2026 (individuals) |

What Happens During the Assessment Year?

- You file your Income Tax Return (ITR) for the income earned in the previous FY.

- You claim deductions, exemptions, and tax credits.

- The Income Tax Department processes your return and may send a refund or raise a demand notice.

- Any scrutiny assessment or notices under Section 143(2) are issued during this year.

- You pay self-assessment tax if any tax remains outstanding after advance tax and TDS.

3. Key Differences: Tax Year vs Assessment Year — Side-by-Side

| Aspect | Tax Year (Financial Year / Previous Year) | Assessment Year (AY) |

|---|---|---|

| Definition | Year in which income is earned | Year in which income is assessed/taxed |

| Period | April 1 to March 31 of the same pair | April 1 to March 31 of the next year |

| Legal term (Income Tax Act) | Previous Year (Section 3) | Assessment Year (Section 2(9)) |

| What happens here? | Income is earned, TDS deducted, advance tax paid | ITR is filed, refunds processed, notices issued |

| Example | FY 2025–26 (Apr 2025 – Mar 2026) | AY 2026–27 (Apr 2026 – Mar 2027) |

| Relevance on ITR form | You select this to refer to income period | You select this on the ITR form dropdown |

| TDS certificates (Form 16) | Covers the FY | Mentioned as AY on top |

| 26AS / AIS | Data reflects transactions of FY | Downloaded while filing during AY |

4. Why is There a One-Year Gap? The Logic Behind It

Many taxpayers wonder — why can’t we just file taxes immediately when the year ends? Why the one-year offset? Here’s the practical logic behind it:

The Government Needs Time to Compute Total Liability

Your income isn’t always fully known on March 31st. Interest income from FDs might credit in April. Capital gains from mutual fund redemptions might be finalized only after a few weeks. Your employer might issue the final Form 16 only in late May or June. The law gives taxpayers and the government time to compile all this information correctly.

Time for Employers and Financial Institutions

Banks need to submit TDS data. Employers need to prepare Form 16. Mutual fund houses need to generate capital gains statements. All these entities have their own timelines — and the law accommodates this by having the assessment happen in the year following the income year.

Historical Origins

The Previous Year → Assessment Year framework was inherited from British-era tax legislation. The concept has remained unchanged even as India has modernized its tax system extensively. The new Income Tax Bill, 2025 does attempt to simplify this terminology — more on that below.

5. Important Tax Dates: FY 2025–26 and AY 2026–27 Timeline

Understanding the FY and AY framework is even more powerful when you map it to actual deadlines. Here’s the key timeline every Indian taxpayer must know for the current year:

6. The New “Tax Year” Concept Under the Income Tax Bill, 2025

This is where things get particularly interesting — and important — for Indian taxpayers in 2025–26 and beyond.

The Indian government introduced the Income Tax Bill, 2025 (also called the New Direct Tax Code) in February 2025. One of its most significant simplifications is the elimination of the confusing “Previous Year” vs “Assessment Year” terminology.

What the New Bill Proposes

- The new bill replaces the concept of “Previous Year” and “Assessment Year” with a single, unified term: “Tax Year.”

- Under the new framework, the Tax Year refers to the period April 1 to March 31 — the same as the current Financial Year.

- Taxes will be assessed for that Tax Year itself — simplifying the terminology significantly.

- So instead of saying “Income earned in FY 2025–26 is assessed in AY 2026–27,” you would simply say “Tax Year 2025–26” for everything.

When Will the New System Take Effect?

As of April 2026, the Income Tax Bill, 2025 has been passed by Parliament but its operational rules are still being finalized. The legacy FY/AY system is expected to be phased out gradually. For ITR filing in AY 2026–27 (for FY 2025–26 income), the old framework still applies. Stay tuned to official Income Tax Department communications for updates.

7. How FY and AY Apply to Your Investments: SIP, Mutual Funds, LTCG, and More

For investors, the FY vs AY framework is not just a naming exercise — it has real financial consequences, especially for capital gains tax.

Equity Mutual Funds and LTCG

Long-Term Capital Gains (LTCG) on equity mutual funds are taxed if held for more than 12 months. The date of redemption falls in a specific FY — and that FY determines which AY you report the gains in.

Example: You redeemed units of an ELSS fund in January 2026. This redemption falls in FY 2025–26. You will report this LTCG in your ITR for AY 2026–27.

SIP Investments and the FIFO Rule

Each SIP instalment is treated as a separate investment for tax purposes. When you redeem SIP units, the FIFO (First In, First Out) method is used. This means SIP instalments from April 2024 complete their 12-month holding period in April 2025 — making them eligible for LTCG treatment if redeemed after that date in FY 2025–26.

Fixed Deposits (FDs) and Interest Income

Interest on FDs is taxable on an accrual basis (not receipt basis) for most taxpayers. This means even if you haven’t received the interest yet, if it has accrued during FY 2025–26, it must be declared in AY 2026–27. Many taxpayers miss this and receive notices from the Income Tax Department.

ELSS Lock-In Period and FY/AY

ELSS investments have a mandatory 3-year lock-in. The lock-in is calculated from the date of each SIP instalment. An ELSS SIP investment made in March 2023 (FY 2022–23) completes its lock-in in March 2026 (FY 2025–26) — meaning you can redeem it and the gains fall in FY 2025–26, to be reported in AY 2026–27.

8. Real-Life Case Study: Riya’s Tax Confusion (and How She Fixed It)

Riya, 32, IT Professional from Pune

Riya is a software engineer earning ₹14 lakhs per annum. She diligently invests ₹5,000/month in SIP mutual funds and ₹1.5 lakhs/year in ELSS for tax saving. In July 2025, she sat down to file her ITR for the first time on the income tax portal without professional help.

The Mistake: On the ITR filing portal, she saw a dropdown asking for “Assessment Year.” Riya thought, “I’m filing for the year I just worked in — April 2024 to March 2025 — so that’s 2024–25.” She selected AY 2024–25. In reality, she should have selected AY 2025–26 (since FY 2024–25 is assessed in AY 2025–26).

The Consequence: Her return was filed for the wrong assessment year. The pre-filled data didn’t match. She received a defective return notice (Section 139(9)) from the Income Tax Department. She had to file a revised return — a stressful process that took another 3 weeks to resolve.

The Fix: Riya learned the “AY = FY + 1” rule. She now writes it on a sticky note on her laptop every June: “Earned income in FY ___ → File ITR in AY ___ (add 1 to FY year).”

The Takeaway: Riya’s mistake is one of the most common ITR filing errors in India. The Income Tax Department receives thousands of such mismatched filings every year. Understanding the FY-AY offset before filing can save you from notices, penalties, and stress.

9. Expert Tips to Never Get Confused Again

10. Common Mistakes to Avoid

Authoritative External Resources

- Income Tax India Official Portal — File your ITR, download AIS, Form 26AS

- Income Tax Act, 1961 — Full text including definitions of Previous Year (Section 3) and Assessment Year (Section 2(9))

- CBDT (Central Board of Direct Taxes) — Circulars, notifications, and tax reform updates

- Ministry of Finance — DEA — Budget documents and Income Tax Bill 2025 updates

11. FAQs — Tax Year vs Assessment Year

12. Conclusion: Never Let Tax Year Confusion Cost You Again

The difference between Tax Year (Financial Year) and Assessment Year is one of those foundational concepts in Indian personal finance that seems trivial — until it causes a very real problem. Getting the AY wrong on your ITR, paying tax against the wrong year, or missing a deadline because of calendar confusion can lead to notices, penalties, and unnecessary stress.

The core principle is elegantly simple: You earn in the Financial Year. You file in the Assessment Year. AY always follows FY by exactly one year. Apply this rule consistently, stay aware of the new Tax Year terminology coming in with the Income Tax Bill 2025, and your tax filing will become dramatically smoother every year.

🎯 Action Step: Before you file your next ITR, write this down: “FY 2025–26 → AY 2026–27.” Put it next to your monitor. Save yourself from Riya’s mistake.

📚 More From Investment Sutras