Teaching Children About Money in India — Age-by-Age Parent Guide 2026

Most Indian parents talk about marks, career, and marriage — but almost never about money. The result? Adults who earn well yet struggle to save, budget, or invest. This guide gives you a practical, age-by-age roadmap to raise a financially confident child — from age 3 to 18.

Paise ki baat karna taboo tha hamare zamaane mein. But that era is over. Today’s children will inherit a world of UPI, crypto, credit scores, and compound interest. If we don’t teach them, the market — or worse, a credit card company — will.

Research from the National Centre for Financial Education (NCFE) shows that financial habits formed before age 12 are among the most persistent throughout life. The good news: you don’t need to be a finance expert to teach your child. You just need to start.

Why Financial Education for Indian Children Matters Now

India has over 600 million people under 25 — one of the youngest populations on earth. Yet SEBI’s investor education surveys show that fewer than 27% of Indians possess basic financial literacy. That number drops further in rural areas and among young adults aged 18–25.

The consequences are visible everywhere: sky-high consumer debt, zero emergency funds, and retirement savings that barely exist. Fixing this starts at home, not in a classroom.

- Children who learn to save before age 10 are significantly more financially stable as adults (Cambridge University, 2013)

- India’s UPI boom makes invisible spending dangerously easy — children need to understand digital money is still real money

- Early exposure to compound interest is the single most powerful investment lesson a parent can give

- Kids who practise delayed gratification are more likely to build long-term wealth

At a Glance: Age-Wise Money Milestones

Money is Real

Coins, notes, exchange — what money is and why we use it.

Save to Buy

Piggy banks, pocket money, needs vs wants.

Budget & Plan

Monthly allowance, expense tracking, savings goals.

Invest & Grow

SIPs, compound interest, credit, income tax basics.

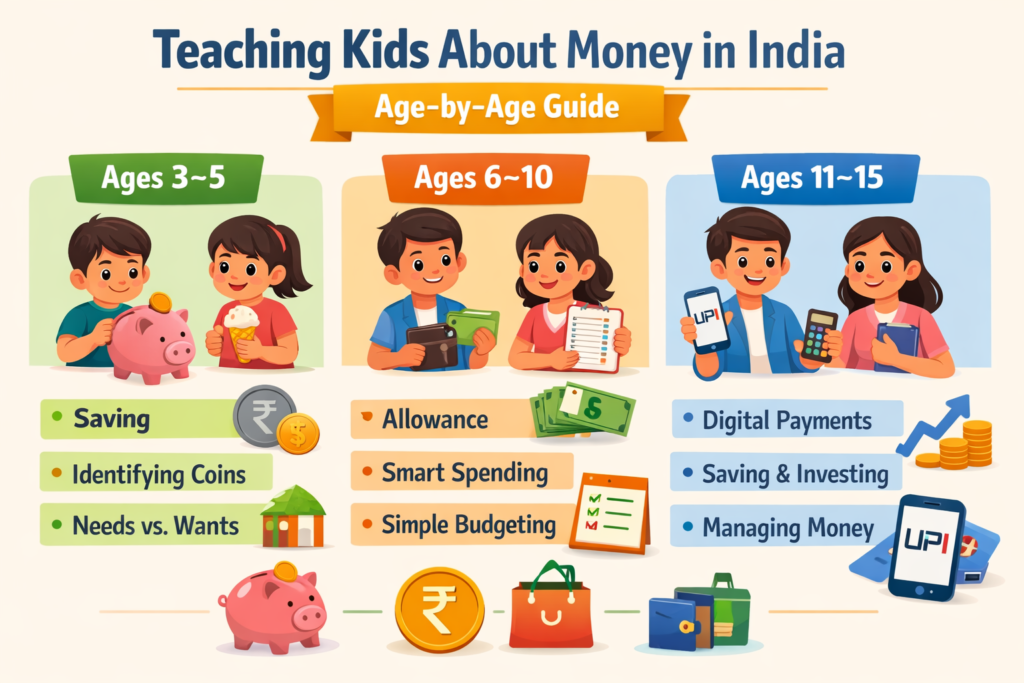

Ages 3–5: Money is Real and Finite

Young children are concrete thinkers. Abstract concepts like “we can’t afford it” mean nothing. What works: things they can see, hold, and count. Your entire job at this stage is to make money tangible.

What to Teach at This Stage

Introduce Coins and Notes by Name

Show them ₹1, ₹2, ₹5, ₹10 coins and ₹10, ₹20, ₹50 notes. Let them sort, count, and stack. Connect each coin to something real: “This ₹5 coin can buy a toffee.”

The Sabzi Mandi Lesson

Take them to the kirana store or vegetable market. Hand them ₹10. Ask them to buy tomatoes. Watch their face when money is physically exchanged for goods. That moment clicks harder than any explanation.

Start a Piggy Bank

Give them a piggy bank — preferably transparent so they can see the coins accumulate. Add ₹2–₹5 coins for small helpful behaviours. Not as bribery, but as introduction to the idea that effort creates money.

Give your 4-year-old ₹10 at the market. Ask them to buy tomatoes priced at ₹5. Teach them to take the ₹5 change and put it back. In one transaction, they have learned: money is limited, exchange is how buying works, and change is what remains. Better than any school lesson.

When children only see you tap a phone and walk away, money feels like magic — unlimited and effortless. Use physical cash sometimes, especially while shopping with them. Let them feel the notes leave your hand.

Ages 6–9: Pocket Money, Saving, and the 3-Jar Method

This is the golden window. Children this age are developing cause-and-effect thinking, they understand delayed gratification in principle, and they care deeply about goals — even small ones like a new cricket bat or a box of LEGO.

How Much Pocket Money in India? (Age-by-Age Guide)

| Age | Suggested Amount | Frequency | Primary Goal | Level |

|---|---|---|---|---|

| 6–7 yrs | ₹20–₹30 | Weekly | Save for a small toy (₹100–₹150) | Starter |

| 8–9 yrs | ₹50–₹70 | Weekly | Practise needs vs wants | Building |

| 10–12 yrs | ₹400–₹600 | Monthly | Budget school & personal expenses | Intermediate |

| 13–15 yrs | ₹800–₹1,200 | Monthly | Full budgeting + savings goal | Advanced |

| 16–18 yrs | ₹1,500–₹2,500 | Monthly | Budget + micro-invest + track spending | Expert |

Note: Amounts vary by city. Mumbai, Delhi, Bengaluru costs are higher. Adjust proportionally — the percentage allocation matters more than the absolute number.

The 3-Jar Method — A Desi Version That Works

Divide every pocket money payment into three jars — physical or digital:

- Spend Jar (50%): For daily needs and small treats — tuck shop, pens, small snacks

- Save Jar (40%): Locked toward a specific goal your child has named. Don’t touch it.

- Give Jar (10%): For charity, a friend’s birthday gift, or helping family. Builds generosity early.

Aryan gets ₹70 every Sunday. He puts ₹35 in Spend (tuck shop + stickers), ₹28 in Save (targeting a ₹280 LEGO set), and ₹7 in Give (his classroom charity box). In 10 weeks, he walks to the toy shop and buys the LEGO himself. That ownership feeling is irreplaceable.

Want to read more about building strong saving habits for your family? See our guide on Best Saving Strategies for Indian Families in 2026.

Ages 10–13: Budgeting, Bank Accounts, and Smart Spending

Pre-teens can handle abstract planning. They understand time, trade-offs, and the future in a real way. Shift from weekly pocket money to monthly allowances. This alone forces better planning.

Needs vs Wants — The Most Important Money Concept Ever

| Needs (buy now) | Wants (can wait or skip) |

|---|---|

| Replacement school bag (bag is torn) | New branded bag just because friends have one |

| Exam stationery — pencils, eraser, scale | Fifth pen set in different colours |

| Monthly bus pass | Ola/Uber to school because it’s raining |

| Lunchbox from home | Dominos in the canteen every Friday |

| Textbooks from library | Buying every book recommended on YouTube |

Open a Bank Account for Your Child

India’s major banks offer dedicated minor savings accounts that are excellent learning tools:

- SBI Pehla Kadam / Pehli Udaan: Zero-balance, debit card with spending limits, online banking access

- HDFC Kids Advantage Account: Linked to parent account, in-app spending controls

- Kotak Junior Account: Excellent mobile app UX, designed for digital-native teens

- Post Office Savings Account (Minor): Great for non-metro families — simple, safe, and government-backed

Opening a bank account at age 11–12 moves the lesson from coins in a jar to real digital money management. Read our full guide: Best Bank Accounts for Children in India 2026.

The Monthly Budget Activity (Age 11+)

Give a Monthly Allowance on the 1st

Switch to monthly. ₹500–₹800 works well for most cities. The longer time horizon forces genuine planning, not just weekly willpower.

Track Every Rupee Spent

Use a physical notebook or a free app like Walnut to log expenses. Review together at month-end. No judgement — just observation.

Set a Named Savings Goal

A ₹1,800 cricket bat, a ₹1,200 novel series — let them pick the goal. When it’s their choice, they’re invested. Review progress monthly.

Let Them Run Out (Once)

If they blow the whole month’s allowance by the 12th and have nothing for the next 18 days — don’t bail them out. This controlled failure, with zero real-world consequences, is more educational than a hundred lectures.

Ages 14–18: Investing, Compound Interest, and Real Finance

Teenagers in India are digital natives watching finance reels on Instagram and YouTube. Many know the word “SIP” but have no idea what it actually does to their money over time. This is your moment to make it real.

The One Example That Changes Teenage Minds Forever

Tell your teenager: “If you invest ₹1,000/month from age 18 at 12% annual returns, by age 40 you’ll have approximately ₹35 lakhs.” Then ask: “What if you wait until 28 to start?” Answer: just ₹9.5 lakhs. Same ₹1,000 per month. Same 12% return. 10 fewer years = ₹25.5 lakh difference. Show them this on the SIP Calculator at InvestmentSutras.com. Watch their expression change.

What to Cover With a 14–18 Year Old

| Topic | Key Lesson | Where to Learn More |

|---|---|---|

| Compound Interest | Money grows on its own growth. Time is the real asset. | InvestmentSutras SIP Calculator |

| Inflation | ₹100 today buys less in 10 years. Money must grow faster than inflation. | MOSPI CPI Data |

| Mutual Funds | Pooled investing managed by professionals. SIP = automated discipline. | Mutual Funds Beginner Guide |

| Credit Cards | Not free money. 36–48% annual interest if unpaid. One of life’s most dangerous tools. | RBI Consumer Education |

| Income Tax | When you earn, part goes to the government. Plan for it from day one of your first job. | Income Tax India Portal |

| Term Insurance | The cheapest way to protect your family. Not an expense — a safety net. | Term Insurance India Guide |

Start a Mutual Fund in Your Teen’s Name

Under SEBI guidelines, parents can hold mutual funds in a minor child’s name with the parent as guardian. Platforms like Groww and Zerodha Coin make this seamless. Benefits:

- Builds a real corpus for college fees (4–5 years away)

- Child sees their NAV move — skin in the game makes the lesson stick

- When the account converts at 18, the child already knows what they own and why

Also consider Sukanya Samriddhi Yojana for daughters — 8.2% tax-free returns with government backing, openable for girls under age 10.

5 Money Mistakes Indian Parents Must Stop Making

Treating Money as a Taboo Subject

Children who grow up in financially silent households either become reckless spenders or anxious avoiders. Neither is healthy. Age-appropriate transparency normalises money conversations.

Using Money as Reward or Punishment

“Score 90% and get ₹500” trains children to see money as validation, not a tool. Reward effort and behaviour. Money lessons should be separate from academic performance.

Buying Everything Without Letting Them Earn or Wait

When children never experience saving for something, they have no framework for it as adults. Small “save for a goal” exercises build the muscle — even if the goal is just a ₹200 toy.

Skipping the Investment Conversation Entirely

Most Indian parents talk about FDs at most. But equity mutual funds, index investing, and the power of starting early are concepts teenagers can absolutely grasp — and act on within a few years.

Making All Payments Digital When Kids Are Watching

UPI makes money invisible. For children under 10, use cash regularly. When the ₹500 note leaves your wallet and doesn’t come back, the lesson of finite resources is immediate and visceral.

- SIP Calculator — See How Your Money Grows Over Time

- Mutual Funds for Beginners in India (2026 Guide)

- Sukanya Samriddhi Yojana — Best Scheme for Your Daughter

- Top Government Saving Schemes for Indian Families — PPF, SSY & More

- How to Budget Your Salary in India — The 50/30/20 Rule Explained

- Best Term Insurance Plans in India 2026 — Full Comparison

Frequently Asked Questions

Start Your Family’s Financial Journey Today

Calculators, guides, and investment strategies designed for Indian families — all in plain language.

Visit InvestmentSutras.com →