Job Gone? Here’s How to Manage Your Finances Smartly in India (2026 Survival Guide)

How to Manage Finances If You Lose Your Job Suddenly in India

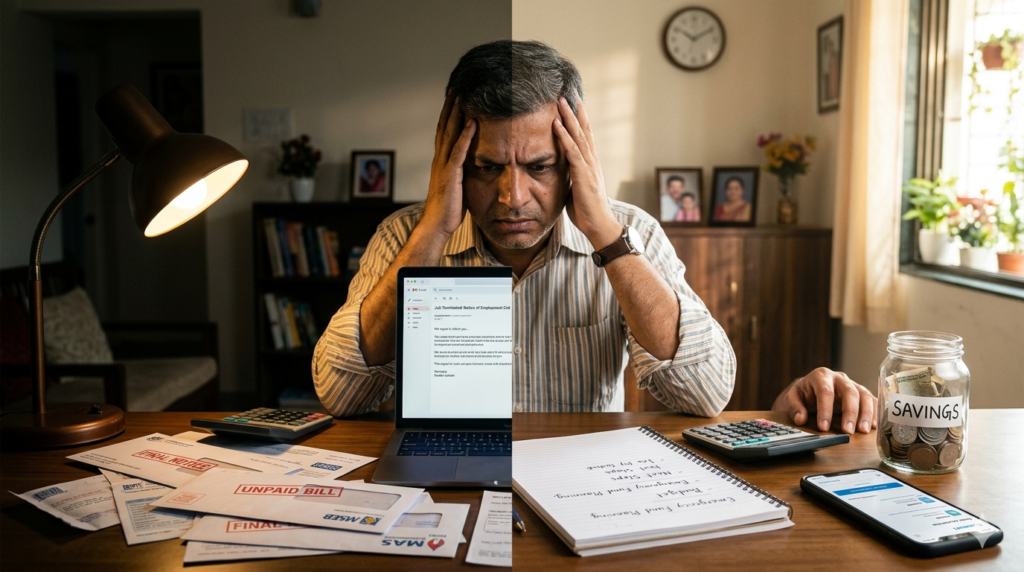

Picture this: It’s a perfectly ordinary Tuesday morning. You’ve already had your chai, you’re dreading a 10 AM meeting, and then — ping — an email from HR with the subject line “Important: Please step into the conference room.”

Twenty minutes later, you’re walking out of the office building with a box of your desk belongings, your laptop surrendered, and your access card deactivated. Your EMI reminder, however, still pops up cheerfully at 9 PM.

Job loss is one of those events that India’s middle-class is never quite prepared for — emotionally or financially. We’re brilliant at planning our kids’ education funds and obsessing over SIP returns, but almost no one has a “what if I lose my job tomorrow?” playbook ready.

The truth? In a country where job security is still a cultural expectation, where families depend on a single income, and where there’s no robust government unemployment insurance, suddenly losing your job can feel like the financial equivalent of jumping out of a plane without a parachute.

But here’s the good news: there is a parachute. You just need to know how to pull the cord. This guide will walk you through exactly how to manage finances after job loss in India — practically, calmly, and with enough clarity to stop your heart from racing every time you check your bank balance.

The First 7 Days: Your Survival Plan

The first week after losing your job is an emotional fog. Your brain will oscillate between “I’ll get a better job by next week” and “I am going to die poor.” Neither is true. What IS true is that the decisions you make in the first seven days set the tone for your entire recovery.

Day 1–2: Don’t Touch Anything (Yet)

Resist every urge to make dramatic financial moves. Don’t withdraw your PF early. Don’t cancel your SIP in a panic. Don’t apply for a personal loan out of fear. Just breathe. Your only job right now is to get clarity on your numbers.

Day 3–4: Understand Your Severance and Exit Terms

Read your offer letter, your HR email, and any exit documentation carefully. You are legally entitled to:

- Notice pay if your employer terminated without serving notice

- Gratuity (if you’ve worked for 5+ years continuously)

- Leave encashment for unused earned leaves

- PF settlement (your contributions + employer’s)

- Any bonuses or variable pay that were earned and unpaid

Many employees in India leave money on the table simply because they don’t ask. Have a calm, professional conversation with HR about all dues. Legally, they must be paid — and knowing exactly what’s coming helps you plan your runway.

Day 5–7: Calculate Your Financial Runway

Your runway is the answer to: “How many months can I survive without any income?” This single number is your most powerful planning tool right now. To calculate it, you need two things: your current cash on hand (savings account + FDs + liquid mutual funds) and your honest monthly essential expenses.

Rohan, a 34-year-old IT project manager in Bengaluru, had ₹4.2 lakhs in savings and ₹85,000 in a liquid fund when he was laid off. His monthly essentials (rent, groceries, utilities, EMI) came to ₹62,000. That gave him a runway of roughly 8 months — enough time to job-hunt without panic-selling his equity mutual funds.

Assessing Your Financial Situation Honestly

Now is the time for radical financial honesty. Not the kind you do at 2 AM when you’re spiralling, but structured, clear-headed assessment. Pull out a spreadsheet, or even a notebook, and list the following:

Assets (What You Have)

- Savings and current account balances

- Fixed Deposits (check lock-in periods)

- Mutual funds — liquid, debt, and equity separately

- PPF, EPF/PF balance

- Stocks and shares

- Gold (physical + sovereign gold bonds)

- Any real estate or rental income

Liabilities (What You Owe)

- Home loan outstanding + current EMI

- Personal loan / car loan

- Credit card outstanding (the dangerous one)

- Any informal loans from family or friends

Monthly Cash Flow Reality

List every single monthly expense — and split them ruthlessly into two columns: Non-Negotiable (rent, groceries, medicine, school fees, insurance premiums, loan EMIs) and Negotiable (OTT subscriptions, dining out, Amazon impulse buys, gym membership you don’t use anyway).

Most Indian households discover that 60–70% of their spending is genuinely non-negotiable. The remaining 30–40% is where your new breathing room lives. Don’t try to eliminate the non-negotiables — focus your energy on trimming the negotiables.

Emergency Fund Strategy: How Much, Where, and How to Use It

If you already have an emergency fund, congratulations — this section is your instruction manual for using it wisely. If you don’t, well, you’ve just learned the most expensive financial lesson of your life. Either way, let’s talk strategy.

How Much Do You Actually Need?

The standard advice is 3–6 months of expenses. But for India specifically — where job searches can take 4–9 months in a senior role, and where “family financial obligations” are a real thing — 6–9 months of expenses is the realistic target.

Liquid Cash First

Keep 2 months of expenses in your savings account. Immediately accessible, no questions asked.

Liquid Mutual Funds

Park 3–4 months of expenses here. Redeemable in 24 hours, better returns than a savings account.

Short-Term FD

Keep remaining buffer in 3-month FDs with premature withdrawal option — earns more, still accessible.

The Golden Rule of Using Your Emergency Fund

Use it only for genuine emergencies — rent, food, medicine, EMIs, school fees. Using your emergency fund to book flights for a “stress-relief” vacation is not a financial strategy; it’s a coping mechanism that will haunt you in month four. Use it with discipline and a clear plan to stop drawing from it the moment any income restarts.

Once you’re back on your feet, build your emergency fund before resuming any investment. The stress of this period is your motivation — use it. Set up an automatic transfer of even ₹5,000/month into a liquid fund the day your new salary hits.

Cutting Expenses Smartly: The Art of Needs vs. Wants in India

Let’s be real. Most Indian households have never actually sat down and done a proper needs vs. wants analysis. The thought of giving up your Swiggy Instamart subscription feels like a personal attack. But tough love time: your budget just got restructured by someone else — now it’s your turn.

| Expense Category | Status | Action |

|---|---|---|

| Rent / Home EMI | NEED | Keep paying. Talk to landlord if needed — many will give 1–2 months grace. |

| Groceries (cooking at home) | NEED | Maintain. Switch to local sabzi mandi from supermarket — save 30–40%. |

| Health insurance premium | NEED | Non-negotiable. Never let this lapse. |

| Children’s school fees | NEED | Priority. Talk to school if needed — most have deferral options for hardship cases. |

| Netflix / Prime / Hotstar | WANT | Pause or cancel all. Free content on YouTube will suffice. |

| Swiggy / Zomato orders | WANT | Suspend. Home cooking is a skill you’re about to rediscover. |

| Gym membership | WANT | Cancel. Walk, run, do pushups. Your body won’t notice the difference, your wallet will. |

| Weekend dining out | WANT | Reduce to once a month maximum. Or a chai at Irani cafe — valid celebration. |

| Car fuel / Uber | Depends | Reduce discretionary trips. Use public transport for non-urgent travel. |

| Term life insurance premium | NEED | Keep paying. This protects your family if the worst happens. |

The goal isn’t to live like a monk. It’s to extend your financial runway by as many months as possible. Even cutting ₹15,000 a month in wants gives you an extra week of runway for every month you do it. Over six months, that’s almost a month and a half of extra time.

Managing EMIs, Loans, and Credit Cards Legally

This is the section most people are too anxious to read — but it’s arguably the most important. Let’s demystify it.

Home Loan EMI

If you have a home loan, contact your bank’s retail lending team proactively. After the COVID-19 pandemic, the RBI established a framework where banks can offer restructuring of loans under genuine hardship. You may be eligible for:

- A moratorium of 1–3 months (interest still accrues, but no payment required)

- Loan restructuring — stretching the tenure to reduce EMI

- Temporary EMI holiday on a case-by-case basis

Do NOT simply stop paying your EMIs without speaking to your bank first. This damages your CIBIL score, attracts penalties, and can have serious consequences. Always communicate proactively — banks strongly prefer a conversation to a default.

Credit Cards: The Real Enemy

If you have outstanding credit card balances, this is the moment to stop using them for anything beyond absolute emergencies. Credit card interest rates in India range from 36% to 48% per annum. This is not a typo. Paying only the minimum due each month is a financial trap that can bury you. If you have the cash, pay down the full outstanding. If not, at minimum avoid adding new spend.

Personal Loans

Personal loans typically have no collateral, making them harder to renegotiate. However, you can still call your lender and explain your situation. Some NBFCs and banks offer a short “hardship pause” for genuine cases. The worst they can say is no — and you’ll still have your relationship intact.

When money is tight, pay in this order: 1) Rent or home loan EMI, 2) Health insurance premium, 3) Groceries and essential utilities, 4) Term life insurance, 5) Children’s school fees, 6) Other loan EMIs. Credit card dues (if any) come last — negotiate with them if needed.

Insurance Considerations: The Two You Cannot Afford to Lose

There are exactly two insurance policies you must protect even while cutting everything else: your health insurance and your term life insurance.

Health Insurance

When you were employed, your company likely provided group health coverage. The day you lose your job, that coverage is usually gone. If you don’t have an individual health insurance policy, you are now uninsured — which in India’s expensive private hospital environment is a single medical emergency away from a financial catastrophe.

Immediately explore a family floater policy if you don’t have one. Even a basic ₹5 lakh cover with a reputable insurer costs around ₹12,000–₹18,000 annually for a family of three (depending on age and city). That is cheap compared to a three-day ICU stay.

Term Life Insurance

If you have dependents — a spouse, children, or parents — your term life insurance is what stands between them and financial ruin if something happens to you during this difficult period. Keep paying the premiums. If the annual premium feels burdensome, remember: letting a term plan lapse means you’d have to buy a new one later at older age and higher premiums, assuming no health issues crop up in the interim.

Use PMJAY (Ayushman Bharat) if you’re eligible — it provides up to ₹5 lakh of health coverage per year for eligible families at zero cost. Check eligibility on the official pmjay.gov.in portal.

How to Generate Temporary Income in India

While you’re job hunting, waiting for the perfect offer is a luxury your bank account may not afford. India in 2025 has a remarkably robust gig economy — and your skills almost certainly have a market outside of a salaried role.

Freelancing and Consulting

Whatever you were paid to do as an employee, someone out there will pay you as a freelancer — often at a higher per-hour rate. Platforms active in India:

- Toptal, Upwork — Tech, design, writing, consulting

- Freelancer.in, PeoplePerHour — Wider range of skills

- LinkedIn — Announce your availability as a fractional consultant (very effective for senior professionals)

- Fiverr — Specific, packaged services (logo design, video editing, content writing)

Gig Economy Roles

This is not below you — it is a bridge. Temporary income is always better than no income, and it keeps your confidence up during a job search.

- Delivery gigs: Swiggy, Zomato, Amazon Flex

- Ride sharing: Ola, Uber (if you own a car)

- Dunzo, Blinkit fulfillment center roles

- Teaching / tutoring: Vedantu, UrbanPro, Superprof

Monetise What You Already Know

- Start a YouTube channel or blog in your area of expertise

- Offer online courses on Teachable, Udemy, or even WhatsApp groups

- Rent a spare room on MakeMyTrip or NoBroker Home Services

- Sell handmade goods or baked items through Instagram or WhatsApp communities

- Offer bookkeeping / accounting freelance services if you have that background

A 40-year-old HR manager from Pune started creating short LinkedIn videos about hiring advice during her job search. Within 8 weeks she had 3,000 followers, two paid consulting calls, and an inbound job offer — all from the same activity. Your expertise is an asset. Start broadcasting it.

Government Schemes and Benefits Available in India

India doesn’t have a formal unemployment allowance scheme like many Western countries. However, there are several safety nets worth knowing about:

- ESIC (Employees’ State Insurance Corporation) — Rajiv Gandhi Shramik Kalyan Yojana: If you were an ESIC-enrolled employee (typically those earning up to ₹21,000/month), you may be eligible for an unemployment allowance equal to 50% of your daily wage for up to 2 years after job loss. Check esic.nic.in for eligibility.

- Ayushman Bharat / PMJAY: Health coverage if you fall into the eligible income bracket post job loss.

- PMEGP (Prime Minister’s Employment Generation Programme): If you are considering starting a small business, this scheme offers subsidised loans through MSME ministry.

- Skill India / PMKVY: Free short-term skill development courses that can add certifications to your profile during the gap period.

- National Career Service Portal (ncs.gov.in): Government job listings and placement services — underutilised but genuinely useful for certain sectors.

- EPF/PF Withdrawal: EPFO allows partial withdrawal for certain purposes. However, think carefully before withdrawing — this is retirement money and the tax and compounding implications are significant.

EPF withdrawal before 5 years of continuous service attracts tax (TDS at 10% with PAN, 34.6% without PAN). More importantly, you lose the power of compounding on your retirement corpus. Only withdraw if it’s a genuine last resort.

Protect Your Investments: Don’t Panic Sell

Here’s a scenario playing out in thousands of homes during a layoff: Markets are volatile, the portfolio is down, the savings are being drained, and the anxiety is unbearable. So the person redeems their equity mutual funds — at a loss — to feel like they have “cash in hand.”

Six months later, the markets recover, they’ve missed the rebound, and they’ve also paid capital gains tax on the redemption. This is the single most common financial mistake people make after a job loss.

The Liquidation Order (Follow This)

- First, use your liquid savings and liquid mutual funds

- Then, short-term debt mutual funds

- Then, FDs (break the smallest ones first, to minimise penalty)

- Only then, consider equity mutual funds — and only if absolutely necessary

- Never break your PPF prematurely (you lose compounding and there are restrictions)

- Never surrender your term or endowment insurance policy unless it’s a true final resort

If you can afford even ₹1,000–₹2,000 a month in a SIP, keep it running. A market downturn during your job loss period is actually an opportunity — you’re buying units at lower prices. If you truly cannot afford it, pause (not cancel) your SIP temporarily.

Mistakes to Avoid During Unemployment

Being forewarned is being forearmed. Here are the most common and costly mistakes people make after sudden job loss in India:

- Taking a personal loan out of panic — Adding debt when you have no income is like bailing water into a sinking boat. Avoid this unless it’s a true emergency with a clear repayment plan.

- Hiding the situation from your spouse or family — Financial stress secrets in a family create worse outcomes than the financial stress itself. Have the honest conversation early.

- Accepting any job offer in desperation — Taking a role that pays 40% less and has no growth path just to end the discomfort often means repeating the job search in 6 months. Be selective, but not endlessly picky.

- Withdrawing from equity investments in a down market — Explained above, but worth repeating: don’t lock in your losses.

- Ignoring your CIBIL score — Even one missed EMI payment affects your credit score. A lower score means higher interest rates on future loans when you do need them.

- Over-spending on “networking” or “looking the part” — Buying a new suit, attending expensive events, upgrading your laptop — unless truly necessary, these are lifestyle inflation disguised as career investment.

- Neglecting mental and physical health — Skipping meals to save money, not sleeping, isolating yourself — these cost more in productivity and recovery speed than they save.

The Psychology of Money Stress: Let’s Talk About It

Here’s something financial articles rarely say: losing your job in India isn’t just a financial crisis. It’s a identity crisis. In a culture where “What do you do?” is the second question after someone learns your name, being unemployed can feel like you’ve temporarily ceased to exist as a person of worth.

The money anxiety is real. Checking your bank balance at 3 AM, doing mental calculations in the middle of a conversation, feeling a knot in your stomach when your phone shows a bank notification — these are genuine stress responses, not weakness.

Practical Psychological Anchors

- Structure your day — Treat your job search like a job. Fixed wake-up time, job-search hours, lunch break, skill development time. Structure prevents the spiral.

- Set a weekly “panic budget” — Allow yourself one hour a week to look at all your numbers and worry formally. Outside that hour, redirect financial anxiety thoughts intentionally.

- Talk to someone who has been through it — Chances are, someone in your network has navigated this. Their lived experience is more valuable than any article.

- Limit doom-scrolling on LinkedIn — Seeing peers post about promotions while you’re between jobs is cognitively painful. You don’t need that fuel on your anxiety fire.

- Celebrate small wins — A callback from an interview, a freelance client acquired, a month of expenses covered from alternative income. These count. Mark them.

Your net worth is not your self-worth. This period will end, and you will look back at it as one of the defining moments that strengthened your financial resilience. Every seasoned professional has at least one chapter of genuine difficulty in their career story. This is yours.

Your Step-by-Step Recovery Roadmap

Here’s how to think about the three phases of financial recovery after job loss in India.

Months 0–3: Stabilise and Survive

Collect all dues from former employer. Calculate runway. Cut discretionary expenses ruthlessly. Contact lenders proactively. File income tax return if due. Start job search immediately — even while you’re processing the situation. Generate even ₹5,000–₹10,000 a month in freelance or gig income to slow down emergency fund drain. Do not touch equity investments.

Months 3–6: Rebuild Momentum

By now you should have a clearer picture of the job market and timeline. Intensify your job search — broaden your criteria slightly if needed. Scale up any freelance income. Reassess your budget monthly. If you haven’t found a role, evaluate whether retraining or consulting makes sense. Keep one hand on your runway number at all times.

Months 6+: Recovery and Reinforce

If a job hasn’t materialised, seriously consider a step-down role or a contract engagement to restart income. When income restarts — whether from a new job or freelance — resist the urge to immediately return to old spending patterns. First: replenish emergency fund. Second: restart SIPs. Third: pay down any debt accumulated. Fourth: normal lifestyle spending resumes. Not the other way around.

Conclusion: You Will Get Through This

If you’ve read this far, you’re already doing better than most. Because the people who manage finances after job loss in India successfully aren’t the ones who had the biggest savings accounts — they’re the ones who stayed calm, got clear on their numbers, made thoughtful decisions under pressure, and resisted the very human temptation to either freeze or overreact.

Job loss is not the end of your financial story. It’s a chapter — a difficult, character-building, occasionally humbling chapter that millions of Indians navigate every year. What defines the outcome is not the event, but the response.

You have more options than you think. You have more resilience than you know. And now, you have a plan.

Share this article with someone you know who might need it. Because the best thing about a good financial survival guide is that it works even better when the people around you have read it too.

Frequently Asked Questions

Found This Useful? Share It.

Someone in your network may be going through this right now and not saying a word. Share this article — it might be the most practical thing you do for them today. And if you found value here, subscribe to InvestmentSutras for more honest, practical personal finance guidance built for India.

Visit InvestmentSutras →- → “

- → “

- → “

- → “

- →

📚 Reference Sources (For Verification)

- Reserve Bank of India (RBI) — Loan Restructuring and Moratorium Guidelines: rbi.org.in

- Employees’ Provident Fund Organisation (EPFO) — PF Withdrawal Rules: epfindia.gov.in

- Employees’ State Insurance Corporation — Rajiv Gandhi Shramik Kalyan Yojana: esic.nic.in

- SEBI — Registered Investment Advisers Directory: sebi.gov.in

- PM Jan Arogya Yojana (Ayushman Bharat): pmjay.gov.in

- National Centre for Financial Education: ncfe.org.in

- National Skill Development Corporation (PMKVY): nsdcindia.org

Disclaimer: InvestmentSutras is an educational initiative. All articles and assessments are for educational and learning purposes only. This should not be treated as investment advice or recommendation. Please consult a registered investment advisor before acting on any suggestions.