Why People Earning ₹1 Lakh Still Live Paycheck to Paycheck in India (2026 Reality Check)

Why People Earning ₹1 Lakh Still Live Paycheck to Paycheck

The uncomfortable truth about high salaries, zero savings, and the financial traps Indian professionals walk into every single month.

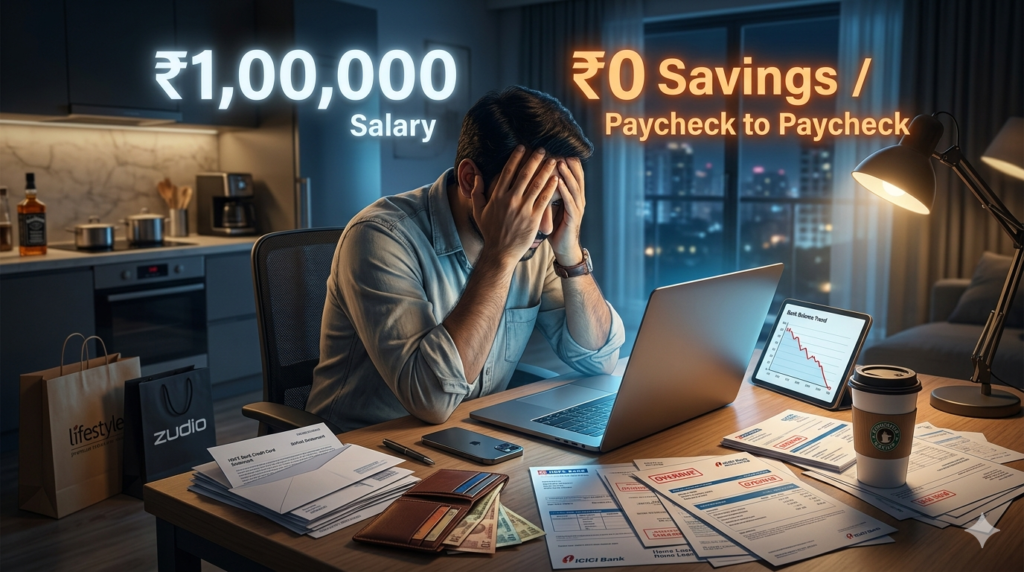

Meet Rahul. He’s 29, works at an MNC in Bengaluru, draws a salary of ₹1,02,000 per month, and still sends his mother a message on the 25th of every month: “Amma, please transfer ₹5,000 — rent is due.”

This isn’t fiction. This is the Wednesday-evening confessional that plays out in millions of WhatsApp conversations across India’s metro cities. The person earning ₹1 lakh a month borrowing money from a parent who makes ₹25,000.

If you’ve ever Googled “earning 1 lakh but still broke in India” — perhaps at 2 AM while staring at a bank balance that looks suspiciously like a phone number — this article is for you. And if you haven’t, forward it to someone who secretly needs it.

The Real Salary Isn’t What You Think

Here’s the first gut-punch of the article. That ₹1,02,000 CTC you negotiated? By the time it hits your account, it’s already been quietly mugged in a dark alley called the Indian tax and deduction system.

Let’s do a quick, realistic breakdown for a Bengaluru-based salaried professional in 2026 — no creative accounting, just the honest numbers:

| Component | Amount (₹) |

|---|---|

| Gross Monthly Salary (CTC/12) | 1,02,000 |

| PF Deduction (Employee – 12%) | 7,200 |

| Professional Tax | 200 |

| TDS (Income Tax – new regime est.) | 8,500 |

| Group Medical Insurance Premium | 900 |

| In-hand Salary | ≈ ₹85,200 |

Right. So the ₹1 lakh person is actually a ₹85,000 person before they’ve even bought a single cup of filter coffee. And yet their lifestyle, their EMIs, their social calendar — all of it was secretly budgeted for ₹1 lakh.

That gap? That’s where the financial bleeding begins.

Most Indians negotiate their CTC but budget based on it. They design their life around a number that was never real. The actual money that arrives is 15–18% lower — and nobody told them to plan for that.

Reason #1: Lifestyle Inflation — The Slowest Thief in the Room

You got a promotion. You earned it. So naturally, you upgraded your phone (EMI), moved to a bigger flat (higher rent), switched from Zepto to Blinkit Premium, and started ordering sushi on Saturdays because “you deserve it.”

This is lifestyle inflation — and it’s so gradual, so normalized, that most people never notice it’s happening. Your salary grew 30% over three years. So did your expenses. The gap between income and savings? Roughly the same as it was when you earned ₹40,000.

The danger isn’t spending money. The danger is that every upgrade feels completely justified in the moment. A ₹15,000/month rent upgrade feels reasonable on a ₹1 lakh salary. So does the streaming bundle, the gym membership, the weekly Swiggy orders. Individually, each makes sense. Together, they quietly consume your financial future.

The Bengaluru Lifestyle Tax (A Rough Monthly Reality)

- Rent in a decent 1 BHK (HSR/Koramangala): ₹22,000–₹28,000

- Groceries + Blinkit + dining out: ₹10,000–₹15,000

- Cab rides / petrol + bike loan EMI: ₹8,000–₹12,000

- Subscriptions (Netflix, Spotify, Hotstar, gym): ₹3,500–₹5,000

- Weekend plans (bars, movies, travel): ₹5,000–₹10,000

We’re already at ₹55,000–₹70,000 — and we haven’t touched EMIs, insurance, or the cousin’s wedding gift yet. Living paycheck to paycheck in India isn’t a poor person’s problem. It’s an everyone problem.

Reason #2: The EMI Trap — Buy Now, Regret Slowly

No Cost EMI. Zero down payment. Pay after 3 months. Indian fintech in 2026 has made debt so frictionless, so guilt-free, so jazzy — that borrowing for things you can’t afford feels like smart financial planning.

It is not.

The average metro professional in 2026 carries 3–5 active EMIs simultaneously: a phone, a laptop, a two-wheeler, perhaps a personal loan taken during a moment of financial optimism, and maybe a BNPL tab that’s been quietly rolling over for six months.

Here’s the brutal math: if 25–30% of your in-hand salary is going toward EMI repayments (which RBI broadly recommends as a ceiling), that’s ₹21,000–₹25,000 of your ₹85,200 already gone. Add rent. Add food. Add the gym you visit twice a month. Congratulations — you’re now high salary but no savings in India, and you’ve earned it.

The Hidden Cost Nobody Counts: Opportunity Debt

Every rupee in EMI is a rupee not compounding in a mutual fund. A ₹15,000/month EMI running for 3 years is ₹5.4 lakhs paid. The same amount invested monthly in a diversified equity fund at a conservative 12% CAGR over the same period? Closer to ₹6.4 lakhs — with a corpus that keeps growing. The EMI ends. The investment would have just started blooming.

Reason #3: Social Pressure — The Most Expensive Peer Group in History

India has a unique financial affliction that no economics textbook covers: the Shaadi-Ghumna-Dikhana Complex.

Your colleague books a trip to Bali. You can’t be the one who stayed home and watched reruns. Your batch-mate is getting married — destination wedding in Goa, and you’re in the wedding party, which means flight, hotel, outfit, gift, and somehow still looking happy for three days. Your friend just posted photos of a weekend brunch at a rooftop restaurant. The caption says “life is short.” The bill, split seven ways, was ₹2,400.

Social spending in urban India is not optional spending. It’s emotionally mandatory. Saying no carries real social costs — missed connections, FOMO, the creeping anxiety of being left out. And so, people who genuinely cannot afford it spend anyway. They put it on a credit card. They tap into whatever tiny buffer they had. And the cycle deepens.

This is why why salary is not enough in India is the wrong question. The real question is: why are we outsourcing our financial decisions to our social circles?

Reason #4: The Tax Inefficiency Nobody Talks About

Most Indian salaried professionals do exactly one thing with their taxes: accept whatever their HR sends them, invest ₹1.5 lakh in some random ELSS at the last minute in March, and call it “tax planning.”

That’s not planning. That’s panic investing.

A ₹12 lakh per annum earner (₹1 lakh/month) in the new tax regime pays roughly ₹52,000–₹60,000 in income tax per year, depending on structure. With even basic optimisation — HRA claims (if on old regime), NPS contributions under Section 80CCD(1B), food coupons, reimbursement structuring — this could be reduced by ₹18,000–₹30,000 annually. That’s an extra ₹1,500–₹2,500 per month sitting on the table, unclaimed, just because no one bothered to ask HR the right questions.

For most salaried Indians, proper salary structuring and tax optimisation is worth more per month than a 5% appraisal. You don’t need a raise to earn more — you need a better relationship with your payslip.

Reason #5: Hidden Expenses — The Budget Vampires

These are the expenses that don’t appear in any budget spreadsheet but show up, faithfully, every month — draining blood without anyone noticing:

- Subscriptions you forgot you had. A 2026 survey of urban professionals found the average person pays for at least two subscriptions they haven’t used in 90 days. That’s ₹800–₹2,000 vanishing silently every month.

- The “convenience premium.” Ordering coffee delivered at ₹180 instead of making it (₹12). Taking an Uber for a 2 km stretch that an auto would cover for ₹60. Multiplied across a month, this adds up to ₹3,000–₹6,000.

- Banking charges and late fees. Credit card late payment penalty (₹500–₹1,200), overdraft charges, and — this one stings — the cash advance fee people pay when they swipe a credit card at an ATM out of desperation.

- Inflation on fixed costs. Your rent went up ₹2,000 this year. Your electricity bill jumped 18%. Your building maintenance increased. None of these were in your original budget. All of them stayed.

- The family contribution that grew silently. What started as ₹5,000/month to parents is now ₹12,000, because inflation hits them harder and saying no feels impossible. This isn’t a complaint — it’s a planning gap.

Reason #6: Psychological Spending — When Your Brain is the Enemy

This is where it gets uncomfortably personal.

Indian professionals — especially those who grew up in middle-class households where money was always tight — carry a complex relationship with wealth. When the first big salary hits, there’s an unconscious urge to signal that the struggle is over. To prove, to yourself and others, that you’ve arrived.

This manifests as conspicuous spending: the brand-name sneakers, the iPhone even when the Android works perfectly, the business-class upgrade that you “treat yourself to” twice a year while your savings account collects digital dust.

There’s also comfort spending — the stress-shopping triggered by a bad day at work, the post-performance-review retail therapy, the impulsive Myntra order at 11 PM because the project deadline was brutal. Emotional spending costs Indian urban professionals an estimated ₹4,000–₹9,000 per month — money spent not out of need but out of feeling.

And then there’s the sneakiest one: “I’ll save what’s left at the end of the month.” Spoiler: there is nothing left. There never is. Because unspent money is not inert — it gets absorbed by the frictionless world of UPI payments, 1-click checkout, and 10-minute delivery.

How to Break the Paycheck-to-Paycheck Cycle in 2026

Enough diagnosis. Let’s talk surgery.

Step 1: Reverse the Savings Sequence

Stop trying to save what’s left. Pay yourself first. The moment your salary lands, automate a transfer — SIP, RD, or even a liquid fund — for a fixed amount. Even ₹10,000/month invested consistently from age 28 becomes ₹1.2 crore by age 50 at a 12% CAGR. The maths don’t care about your excuses.

Step 2: Build the “Anti-Lifestyle-Inflation” Rule

Every time you get a raise, allocate at least 50% of the increment to savings/investments before you upgrade anything. If your salary goes up by ₹10,000, ₹5,000 goes to a new SIP. The remaining ₹5,000 can be “lifestyle.” This one rule, compounded over a decade, separates the wealthy from the salaried.

Step 3: Conduct a Subscription Autopsy

Go through your last three months of bank statements and credit card bills. Highlight every recurring charge. Cancel anything you haven’t used in 60 days. Renegotiate the rest. This is not about being cheap — it’s about being intentional.

Step 4: Get Aggressive With EMI Hygiene

Set a personal rule: total EMIs should never exceed 20% of in-hand salary. If you’re at 35%, that’s a financial emergency in slow motion. Prioritise prepayment of high-interest debt (personal loans, credit card rollovers) before anything else. The guaranteed return on prepaying a 16% personal loan is — wait for it — 16%. No mutual fund promises that.

Step 5: Create a “Social Budget” and Stick to It

Decide, in advance, how much you will spend on social activities per month. Let’s say ₹6,000. When it’s gone, it’s gone. Learn to say “I’m on a budget this month” — it’s the most adult sentence in the English language, and nobody actually judges you for it. The ones who do are also broke.

Step 6: Restructure for Tax Efficiency

Book a one-hour session with a fee-only financial planner or CA. Ask specifically about HRA optimisation, NPS benefits under 80CCD(1B), and salary restructuring with food coupons and reimbursements. For ₹500–₹2,000 in advisory fees, you could unlock ₹15,000–₹30,000 in annual tax savings.

Step 7: Build a 3-Month Emergency Fund First

Before investing in equities, before the crypto experiment, before anything — build a liquid emergency buffer of 3× your monthly expenses in a high-yield savings account or liquid mutual fund. This is your financial immune system. Without it, every unexpected expense becomes a financial crisis.

Key Takeaways

- Your in-hand salary is 15–18% lower than your CTC. Plan your life around the real number.

- Lifestyle inflation is invisible and cumulative — it grows with every raise if you let it.

- EMIs feel like affordability; they are actually future income borrowed at a cost.

- Social spending is emotionally real but financially lethal without a fixed budget for it.

- Proper tax planning can add ₹1,500–₹2,500 to your effective monthly income without a raise.

- Saving what’s left never works. Automate savings the day your salary arrives.

- An emergency fund is not optional — it’s the foundation of every other financial goal.

Your 30-Day Action Plan — Start This Week

- Calculate your actual in-hand salary and build your budget around that number only.

- Run a subscription audit: review 3 months of statements and cancel unused services.

- Set up an automatic SIP or RD for the day after your salary credit date.

- List all active EMIs and calculate your total EMI-to-income ratio.

- Create a dedicated “social fund” envelope (digital or physical) for the month.

- Book a one-hour session with a fee-only CA to review your salary structure and tax setup.

- Open a separate savings account or liquid fund account labelled “Emergency Fund” and start contributing ₹5,000/month minimum.

- Commit to the 50% increment rule: the next time you get a raise, invest half before you upgrade anything.

The ₹1 Lakh Earner Who Wins Is the One Who Plans First

Earning ₹1 lakh is a privilege. Spending it all is a choice. And between those two facts lies every financial outcome you will ever experience.

The paycheck-to-paycheck trap is not a salary problem. It’s a systems problem — and systems can be redesigned. Start with one change this week. Then another. The compounding of good financial habits is just as powerful as the compounding of money.

You didn’t grind to a ₹1 lakh salary to stay broke. Build the plan that matches the income.

Explore More Insights at InvestmentSutras.com →If this felt like someone was reading your bank statement — you know what to do. Tag a friend who needs this. 👇

Follow investmentsutras.com for weekly insights on personal finance built for real Indian professionals — not textbook characters.

Disclaimer: InvestmentSutras is an educational initiative. All articles and assessments are for educational and learning purposes only. This should not be treated as investment advice or recommendation. Please consult a registered investment advisor before acting on any suggestions.